The report titled “The India – UK FTA: Implications for Pakistan” is part of the Market Access Series 2025-26 published by the Pakistan Business Council (PBC). This report examines the potential effects of the proposed Free Trade Agreement between India and the United Kingdom on bilateral trade, on Pakistan’s economy, trade competitiveness, and strategic positioning. It highlights key areas of concern and opportunities for Pakistan, including shifts in export markets, investment flows, and regional trade dynamics.

Major Features of the UK, India FTA

The United Kingdom and the Republic of India concluded negotiations on a Comprehensive Free Trade Agreement (FTA) on 6 May 2025. The agreement was subsequently signed on 24 July 2025. Alongside the FTA, both nations have agreed to negotiate a Double Contributions Convention (DCC), which will come into force in line with the wider trade deal.

The United Kingdom and the Republic of India concluded negotiations on a Comprehensive Free Trade Agreement (FTA) on 6 May 2025. The agreement was subsequently signed on 24 July 2025. Alongside the FTA, both nations have agreed to negotiate a Double Contributions Convention (DCC), which will come into force in line with the wider trade deal.

Through this deal, India will remove or reduce tariffs on 90% of tariff lines, covering 92% of existing goods imports from the UK. India on the other hand will cut tariffs worth approximately €400 million annually, which is projected to more than double to around €900 million after ten years of staging.

| Metric |

UK Commitment (to India) |

India Commitment (to UK) |

| Tariff lines liberalized |

99% |

90% |

| Trade value covered |

100% of India’s exports to UK |

91–92% of UK’s exports to India |

| Immediate duty elimination |

99% of tariff lines eliminated at entry into force |

64% of industrial tariff lines immediately; many sensitive lines excluded or staged |

| Phased elimination (5–10 years) |

Minimal — UK’s liberalization is largely front-loaded |

36% of tariff lines staged, e.g. textiles (5–7 yrs), motor vehicles (8 yrs), processed seafood (5 yrs) |

| TRQs |

Not a significant feature |

Applied to sensitive/strategic lines — Scotch whisky, automobiles (ICE & EV), basmati rice |

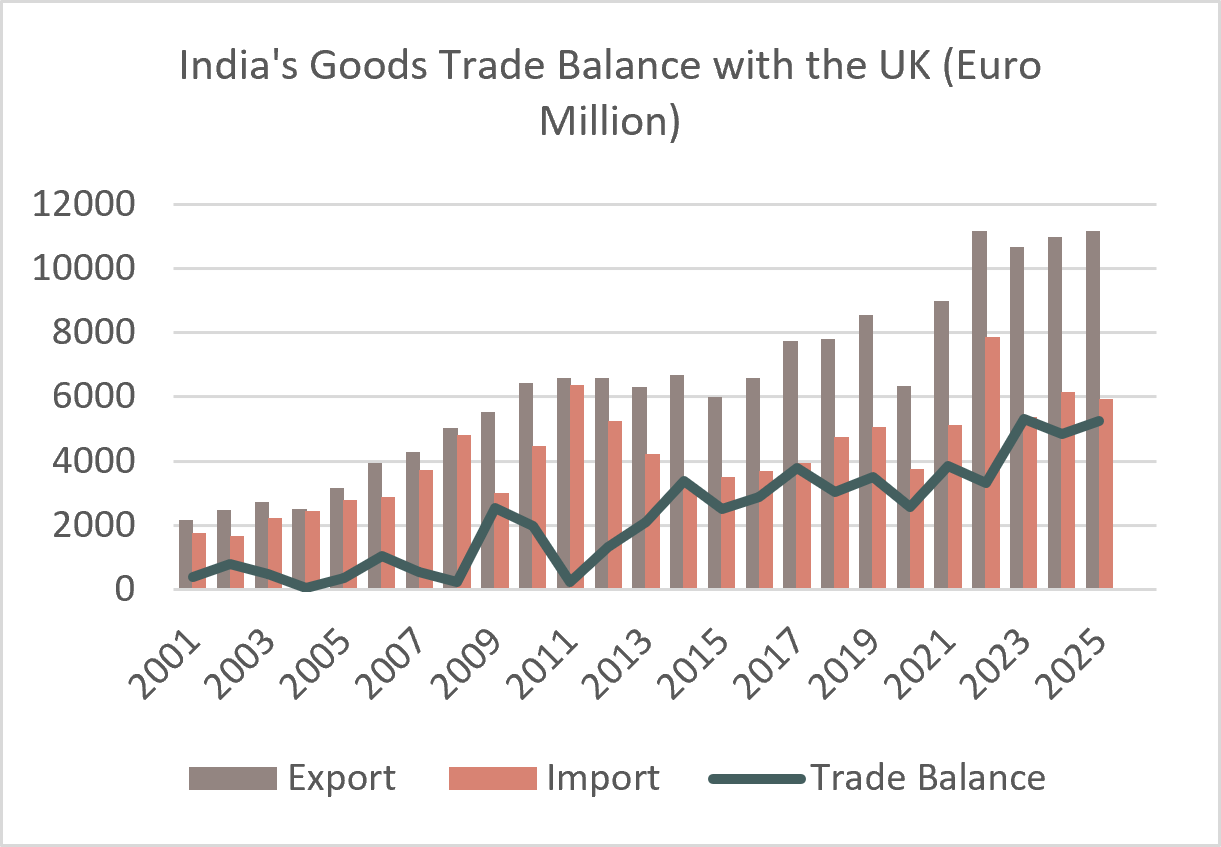

The United Kingdom and Pakistan

The trade relationship between Pakistan and the United Kingdom is robust and growing, with bilateral trade reaching a record high of over €5.5 billion, establishing the UK as Pakistan’s third-largest export destination and its most significant economic partner in Europe. This partnership is characterized by a strong UK investment presence, with more than 200 British companies operating in Pakistan and contributing over €3 billion in investment, playing a vital role in employment, technology transfer, and tax revenues.

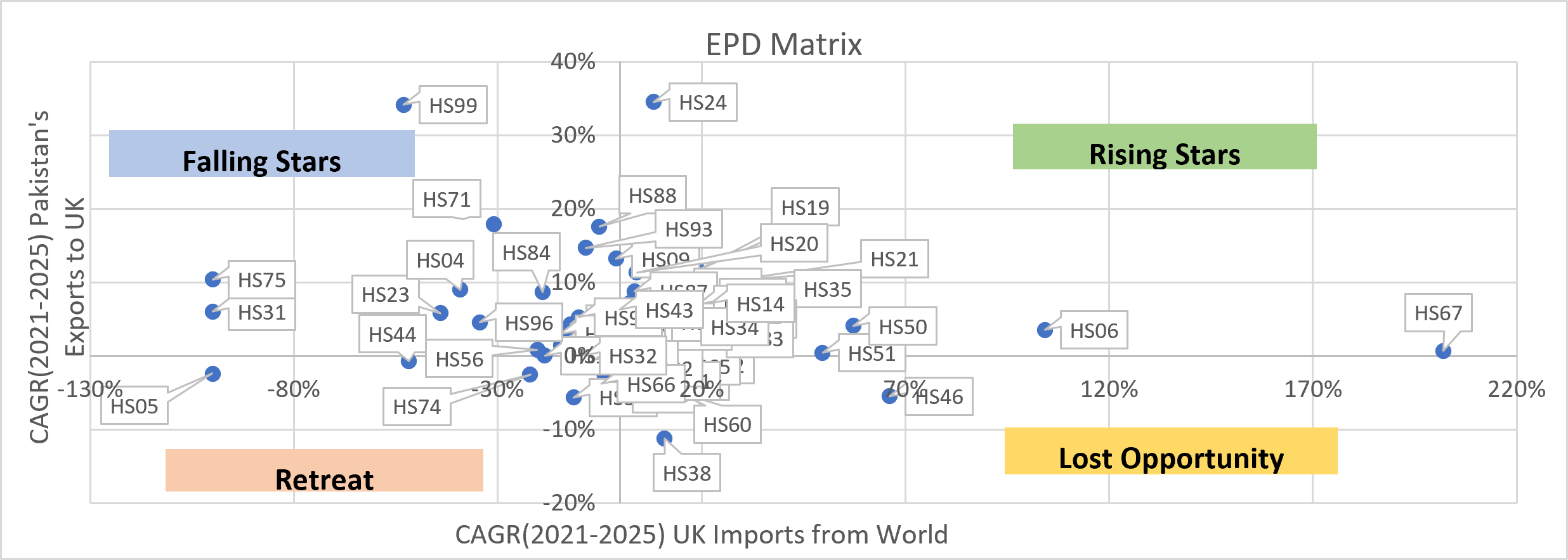

Export Portfolio Diversification (EPD) Matrix

The Export Portfolio Diversification (EPD) Matrix is a tool used to evaluate the performance and potential of export products across different markets.

- Rising Stars (28 sectors): Pakistan is capturing market share in a growing UK market, led by a structural pivot from raw textiles toward value-added agribusiness and high-tech sectors like electrical machinery (+23%) and pharmaceuticals (+13%).

- Lost Opportunity (8 sectors): Despite a contracting overall UK import market, Pakistani suppliers successfully expanded their market footprint in home textiles (+1%), iron/steel (+12%), and resilient niche segments.

- Retreat (10 sectors): Capital is naturally migrating away from low-value, raw commodities (like raw cotton and fibers) as both UK demand and Pakistani production contract in tandem toward an orderly structural phase-out.

- Falling Stars (22 sectors): Trade policymakers face severe competitive erosion in expanding UK markets, marked by declining shares in core agribusiness (rice, spices, dairy) and critical heavy manufacturing (machinery, aviation, aluminum).

Table 1: Pakistan’s Competitive Advantages in the UK Market

Tariff Advantage

10-12% duty-free access under DCTS, providing a temporary price edge over Indian textiles. |

Sports Monopoly

Sialkot cluster produces 70% of the world’s hand-stitched footballs—a niche India doesn’t compete in. |

Surgical Precision

Reliable €34.9 million annual exports in medical instruments with deeply rooted manufacturing expertise. |

Agile Production

Superior cotton quality & lower MOQs preferred by boutique British fashion brands. |

Key Findings:

- The India-UK FTA facilitates significant tariff liberalization on premium British commodities. India will immediately reduce its import duties on Scotch whisky from 150% to 75%, alongside a structured reduction in automotive tariffs—historically capped at 110%—down to 10% under a preferential tariff rate quota (TRQ) mechanism.

- UK companies get a special shortcut to bid on Indian government contracts. They will get preferred treatment as long as 20% of their product comes from the UK. However, this deal only covers the central government, completely leaving out India’s massive state-level public spending.

- The deal fails to help the UK’s strongest sector: financial services. Foreign ownership in Indian banks and insurance firms remains permanently capped at 74%, and India has refused to loosen its strict licensing rules for foreign banks.

- Trade patterns are changing fast. Indian smartphone exports to the UK went from zero to €1.2 billion in just a few years. Meanwhile, pearls have surprisingly become the UK’s single largest export to India, peaking at €6.2 billion.

- British investment into India doubled in a single year, making the UK India’s fourth-largest source of foreign funding. At the same time, the number of Indian-owned businesses operating inside the UK grew by 60%, pulling in nearly €106 billion in revenue.

- Pakistan-UK trade has hit an all-time high of over €5.5 billion, making the UK Pakistan’s third-largest export market. More than 200 British companies are active in Pakistan, contributing nearly €3 billion in investment.

- On the basis of the DCTS – UK’s trading scheme, 94% of Pakistani goods enter the UK tax-free, saving local exporters around €120 million a year. The remaining 6% face standard global taxes.

- To sell to top British retailers, Pakistani factories must prove they follow international standards (like organic or sustainable cotton rules). However, the high cost of getting these official certificates blocks smaller Pakistani firms from competing.

- Pakistan relies on just four markets—the US, EU, UK, and China—for 60% of its entire export economy. This concentration makes Pakistan highly vulnerable if any of these nations decide to change or cancel their trade favor schemes.

Recommendations

- Move from a basic proposal to active negotiations for a formal Free Trade Agreement. This locks in permanent, guaranteed trade benefits instead of relying on temporary, one-sided UK preference schemes (like the DCTS).

- Create a government grant to help medium-sized textile and clothing companies pay for international environmental and labor certifications. This will help them meet the strict standards required by British retailers.

- Set up a monitoring team to watch how the new India-UK trade deal changes British regulations. This ensures new labeling rules or standards do not quietly push Pakistani goods out of the market.

- Use Pakistan’s embassy network & the Pakistani diaspora in London to connect local food brands with major UK supermarkets. Fast-growing sectors like processed foods (+29%) and bakery products (+19%) face fewer border checks than raw crops and have massive growth potential.

- Stop relying permanently on one-sided trading favors from foreign governments, which can be canceled at any time. Instead, focus long-term policy on cutting domestic manufacturing costs, improving shipping logistics, and making Pakistan genuinely competitive on its own merits.

The PBC is a private sector not-for-profit advocacy platform set-up in 2005 by 14 (now 100+) of Pakistan’s largest businesses. PBC’s research-based advocacy supports measures which improve Pakistani industry’s regional and global competitiveness. More information about the PBC, its members, objectives and activities can be found on its website: www.pbc.org.pk

Download