The report titled “The India – EU FTA: Implications for Pakistan” is part of the Market Access Series 2025-26 published by the Pakistan Business Council (PBC). This report examines the potential effects of the Free Trade Agreement between India and the European Union on Pakistan’s economy, trade competitiveness, and strategic positioning. It highlights key areas of concern and opportunities for Pakistan, including shifts in export markets, investment flows, and regional trade dynamics.

The European Union and India

On January 27, 2026, India and the EU finalized a historic FTA at the 16th India-EU Summit in New Delhi, concluding negotiations that began in 2007. The agreement creates a free trade zone of nearly 2 billion people with a combined market of over €22 trillion, accounting for one-fifth of global GDP and one-quarter of the world’s population. With bilateral goods trade already at €120 billion annually (plus €59.8 billion in services), the FTA is expected to double EU goods exports to India by 2032. This agreement represents the most ambitious trade liberalization India has ever granted and one of the largest trade agreements ever negotiated.

On January 27, 2026, India and the EU finalized a historic FTA at the 16th India-EU Summit in New Delhi, concluding negotiations that began in 2007. The agreement creates a free trade zone of nearly 2 billion people with a combined market of over €22 trillion, accounting for one-fifth of global GDP and one-quarter of the world’s population. With bilateral goods trade already at €120 billion annually (plus €59.8 billion in services), the FTA is expected to double EU goods exports to India by 2032. This agreement represents the most ambitious trade liberalization India has ever granted and one of the largest trade agreements ever negotiated.

In August 2025, the US imposed punitive tariffs of up to 50% on 70% of Indian exports—including textiles, auto parts, steel, gems, pharmaceuticals, and chemicals—due to India’s Russian oil imports. The Kiel Institute estimated this would reduce India’s output by 1.64% (≈€53 billion annually). Meanwhile, the US also threatened tariffs on European goods in early 2025 over Greenland-related disputes, prompting India-EU collaboration.

The agreement provides unprecedented market access on both sides, with the EU eliminating tariffs on over 90% of tariff lines (99.3% by value) and India eliminating tariffs on 86% of tariff lines (96.6% by value). Overall, the tariff reductions will save around €4 billion per year in duties on European products.

| Metric |

EU Commitment |

India Commitment |

| Tariff lines liberalized |

Over 90% |

86% |

| Trade value covered |

99.3% |

96.6% |

| Immediate duty elimination |

70.4% of India’s exports (90.7% by value) |

49.6% of tariff lines |

| Phased elimination (3-10 years) |

20.3% of tariff lines |

39.5% of tariff lines |

| TRQs |

6.1% of tariff lines |

3% of products |

| Sources: European Commission, Government of India |

The European Union and Pakistan

The EU is Pakistan’s third largest export destination and second-largest trading partner overall. Total bilateral trade stood at approximately €12 billion in 2025. Pakistan’s exports to the EU reached €8.69 billion in 2025. Since 2014, Pakistan has benefited from the EU’s GSP+ scheme, which grants duty-free access to approximately 66% of its tariff lines.

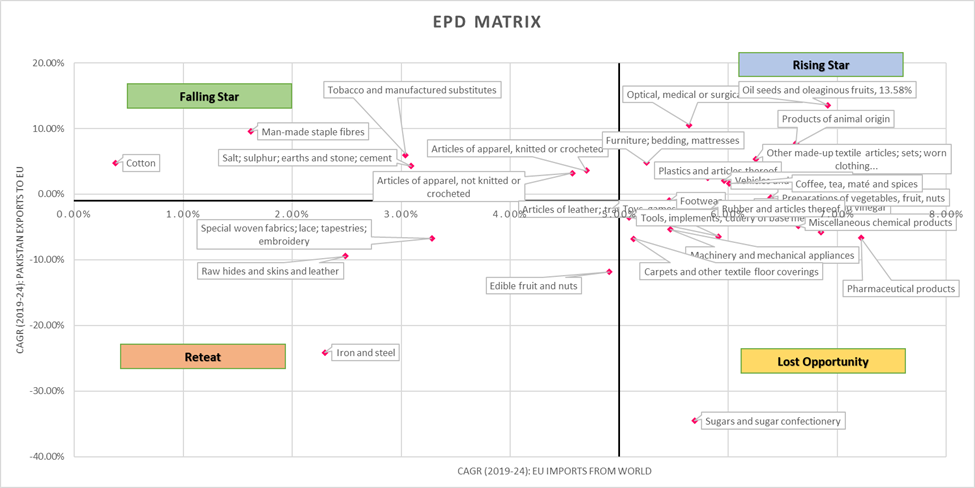

Export Portfolio Diversification (EPD) Matrix

The Export Portfolio Diversification (EPD) Matrix is a tool used to evaluate the performance and potential of export products across different markets. The EPD Matrix below represent the analysis of the products with import value greater than €10 million on the HS-02 Level.

Rising Stars (High EU & Pakistan growth), led by textile articles (HS 63) and niche sectors like medical instruments (HS 90), are Pakistan’s top priority for investment. Lost Opportunities (High EU growth / Low Pakistan growth), including pharmaceuticals (HS 30) and machinery (HS 84) reveal critical underperformance in fast-growing EU markets. Falling Stars (Low EU growth / High Pakistan growth): mainly traditional textiles like cotton (HS 52) serve as stable cash cows needing efficiency and market defense. Retreat (Low EU & Pakistan growth) such as iron and steel (HS 72) and raw hides (HS 41) represent declining sectors with little strategic value.

Key Findings

- Pakistan is the world’s largest beneficiary of the GSP+ scheme. Approximately 86% of its exports to the EU use these preferences, with a 95% utilization rate. This creates a “single-point-of-failure” risk; any change in GSP+ status would immediately jeopardize a significant volume in trade.

- With the India-EU Free Trade Agreement finalized in early 2026, India’s current 12% tariff disadvantage in textiles is being phased out. Once India reaches zero-duty access, Pakistan will lose its tariff edge unless it improves quality and sustainability.

- Pakistan has worked on improving its regional industrial competitiveness by implementing a major tariff reform in February 2026. By reducing electricity rates from a high of 11.9 Euro cents/kWh (which caused 150+ factory closures) to approximately 7.9–8.1 Euro cents/kWh. The revised tariffs are however officially notified to remain in effect only until December 31, 2026.

- A critical layer of uncertainty is the expiration of Pakistan’s current GSP+ scheme in December 2027. This creates a “cliff-edge” scenario:

- Scenario 1 (Renewal with Conditions): Even if GSP+ is renewed, Pakistan will face continued compliance costs and periodic reviews, while India enjoys unconditional FTA access. The playing field will be tilted in India’s favor on certainty, if not on tariffs.

- Scenario 2 (Non-Renewal): If GSP+ is not renewed, Pakistan’s exports to the EU would revert to Standard GSP (with partial preferences) or Most Favored Nation (MFN) terms, facing duties of approximately 9–12%. In this scenario, Indian goods would have a 9–12% price advantage over Pakistani goods in the EU market.

- Foreign Direct Investment (FDI): The India-EU FTA acts as a powerful magnet for investors, offering a stable, rules-based framework and access to a massive market. With 6,000 European companies already in India and goals to double bilateral trade, European firms are “preparing for a post-ratification phase” by expanding manufacturing in India.

Recommendations

- Pakistan must stop futile comparisons with India and pivot inward, focusing on what it can uniquely offer the world. The India-EU FTA signals that relying on tariff preferences is outdated; instead, Pakistan needs a competitive, diversified export sector through energy cost reduction, compliance upgrades, market diversification, and securing GSP+ beyond 2027. Competitiveness, not fear, is the only durable defence.

- Pakistan’s heavy reliance on cotton-based textiles (over 70% of exports) ignores the market reality that man-made fibers (MMF) now account for 74% of global fiber consumption. Shifting to MMF would break the climate-vulnerable “Cotton Trap,” reduce water footprints, and open high-value technical textile markets like medical gowns and automotive airbags—diversifying exports beyond shrinking traditional apparel segments.

- Pakistan must launch an urgent diplomatic offensive to secure GSP+ renewal beyond 2027 by demonstrating compliance with 32 EU conventions and negotiating for ‘Single Transformation’ rules to access high-growth MMF segments. Resources should shift from declining products (basic bedlinen) to high-demand categories like athletic wear and medical textiles, while institutionalizing factory-level labor and environmental monitoring to pass the 2026 EU inspection.

- Creating sector-specific credit guarantee schemes for high-potential export industries: Commercial banks often refuse to lend to exporters, especially in new or “high-potential” sectors (like IT, engineering, or pharmaceuticals) because they view them as risky. A credit guarantee scheme acts as a government-backed safety net. Pakistan already has the SME Asaan Finance (SAAF) scheme. This concept can be extended and refined specifically for “Export to EU” sectors, requiring less fiscal outlay than a bank and providing immediate liquidity to high-growth areas.

The PBC is a private sector not-for-profit advocacy platform set-up in 2005 by 14 (now 100+) of Pakistan’s largest businesses. PBC’s research-based advocacy supports measures which improve Pakistani industry’s regional and global competitiveness. More information about the PBC, its members, objectives and activities can be found on its website: www.pbc.org.pk

Download