Africa represents one of the most consequential emerging economic frontiers of the 21st century. With 55 recognized countries, a population exceeding 1.5 billion, expanding urbanization, rising consumption patterns and abundant natural resources, the continent has increasingly attracted strategic and commercial engagement from global and regional powers. This report examines Africa’s economic profile, compares Pakistan and India’s diplomatic and trade engagements with the continent, analyses current trade structures, and identifies sectors with realistic export potential for Pakistan.

Africa’s Economic Profile and Strategic Importance

Africa is characterized by a 1.5 billion strong population, growing trade volumes, and increasing integration into global markets. The continent’s population growth rate exceeds 2%, significantly outpacing both India and Pakistan’s.

North African economies generally exhibit higher per capita incomes and stronger human development indicators, while Sub-Saharan Africa accounts for the bulk of the continent’s population and potential for trade expansion.

Africa’s economic structure reflects a combination of primary resource extraction and expanding services and industrial sectors. The continent holds approximately 30% of the world’s mineral reserves, including critical minerals essential for modern technologies. Simultaneously, rising urbanization and infrastructure development are driving demand for manufactured goods, pharmaceuticals, construction materials and consumer products.

The continent is, additionally, characterized by its many regional economic blocs, many with overlapping memberships and varying degrees of integration and operationalization.

Diplomatic and Economic Engagement: Pakistan vs India

A central finding of the report is the disparity between Pakistan and India in the depth and breadth of engagement with Africa. While both countries share historical linkages with parts of the continent, India has institutionalized its Africa outreach through sustained high-level diplomacy, concessional credit lines, development cooperation initiatives and extensive private-sector participation.

Pakistan, by contrast, has historically maintained more limited diplomatic coverage and commercial outreach. Although recent initiatives under the “Look Africa” and “Engage Africa” frameworks indicate renewed interest, the scale of engagement remains modest. Pakistan’s aggregate trade with Africa is significantly smaller than India’s, reflecting both structural economic differences and institutional limitations.

Current Trade Patterns and Structural Imbalances

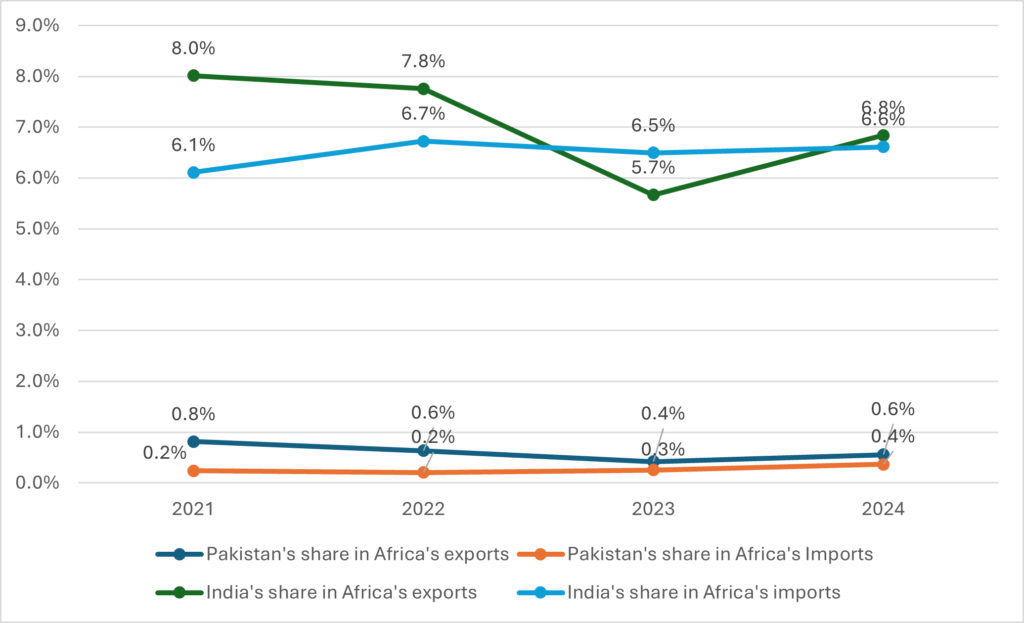

Figure: Pakistan & India’s shares in Africa’s exports & imports

Source: ITC Trade Map

Pakistan’s trade with Africa has grown in recent years, with exports increasing at a compound annual growth rate of 11.3% since 2020. However, export structure reveals significant concentration. 61.9% of Pakistan’s exports to Africa consist of semi- or wholly-milled rice, broken rice and worn clothing. Together, these categories account for a disproportionate share of total export value indicating limited integration into higher value-added manufacturing segments.

In contrast, India’s export profile to Africa is markedly diversified. Its leading exports include refined petroleum products, motor vehicles, construction machinery, pharmaceuticals, vaccines and electronics.

Another structural issue is the mismatch between Pakistan’s global export strengths and African import preferences. While textiles form a dominant share of Pakistan’s global exports, Africa does not represent a particularly large market for these categories. India’s export mix, on the other hand, aligns more closely with African demand for fuels, transport equipment, machinery and pharmaceuticals.

Geographically, Pakistan’s export footprint in Africa remains limited, with insufficient penetration into wealthier and more industrialized markets in North Africa and major sub-Saharan economies. India has achieved stronger presence in markets such as South Africa, Nigeria, Kenya and Tanzania, reflecting sustained commercial engagement and regulatory adaptation.

Sectoral Potential and Strategic Opportunities

The report identifies several sectors where Pakistan has the potential, whether due to favourable demand-side tailwinds or existing production capacities, to meaningfully scale up exports and penetrate new markets in the medium and long terms.

Pharmaceuticals

Africa’s growing disease burden, population expansion and underdeveloped local manufacturing capacity generate substantial demand for generic pharmaceuticals with market demand slated to reach 9,290.0 USD Mn by 2030. Pakistan possesses manufacturing capabilities in generic medicines and can leverage its existing production base along with regulatory harmonization, quality certifications and sustained marketing efforts to compete effectively with established suppliers, particularly India.

Plastics and Manufactured Goods

Industrial expansion and urbanization drive demand for plastics and intermediate goods, with the continent importing 28,349.3 USD Mn worth of plastics in 2024. Pakistan’s domestic production capacity provides scope for expanding exports, considering the relative absence of India from this sector, provided cost competitiveness and logistical efficiency are improved.

Copper and Articles of Copper

Africa’s copper imports have grown steadily, rising to 5,731.4 USD Mn in 2024, particularly in refined copper cathodes and wires. Although Pakistan’s current presence in this segment is negligible, expected investments in mining, extraction and logistics combined with additional smelter and electro-refining facilities could position the country to capture emerging demand linked to infrastructure and renewable energy development.

Livestock and Meat

Africa’s rising meat consumption presents opportunities in livestock, frozen and value-added meat products, with the continent importing 1,647.5 USD Mn worth of livestock and 4,963.7 USD Mn worth of meat in 2024. Pakistan’s experience with halal exports to the Gulf and expanding cold-chain investments create potential entry points pending compliance with diverse sanitary and veterinary standards.

Cement and Clinker

Rapid urbanization and infrastructure projects across the continent sustain demand for cement and clinker, with the continent importing 1,239.5 USD Mn worth of cement and 1,454.9 USD Mn worth of clinker in 2024. Pakistan has recorded growth in cement and clinker exports to Africa holding a measurable but modest market share. Further strengthening competitiveness would entail enhancing port mechanization and reducing freight costs.

Surgical Instruments

Pakistan’s established surgical instruments sector offers potential, though exports to Africa only constituted 3.6% of global sales for Pakistan. Pakistan has a strong case for its exports in the North, South and East African markets pending improvements in domestic logistics, direct shipping and improved brand marketing.

Rice

Rice exports have performed strongly, benefiting from competitive pricing and regional demand, with exports to Africa surging to 942.6 USD Mn in 2024. With inroads into the African market made in India’s absence, Pakistan has significant potential for ramping up exports, contingent on reduced costs.

Stakeholder Engagement

As part of the report, stakeholders represented by appointed trade officers/attaches, exporters and experts with insight into the African space were interviewed regarding the opportunities and challenges faced by Pakistan in the African market and their observations and recommendations are included in the study.

- Orient private sector interest towards Africa by sponsoring African delegations to build B2B rapport and offer diversity and professional conduct training sessions for Pakistani exporters.

- Reduce transport costs and times by expediting direct shipping routes between Karachi and Mombasa and Djibouti, upgrading port mechanization and rationalizing port tariffs in line with regional peers.

- Bolster commercial and diplomatic presence in the country by intensifying diplomatic engagements, participating in African-delegate-attended trade fairs and pursuing joint venture in domains of Pakistani expertise.

- Improve trade financing by signing re-insurance treaties between EXIM Pakistan and global re-insurers and expanding product offerings to include buyer’s credit, working capital finance and sector specific products.

- Improve business mobility by pursuing G2G cooperation to introduce e-Visa facilities for exporters and investors, expanding diplomatic missions and conducting feasibility studies for direct flights between underserved destinations.

- Prioritize the resolution of non-tariff barriers including logistics, business networking, trade financing, mobility restrictions, and diplomatic and commercial presence over negotiating trade pacts solely for tariff relief.

- Improve bilateral business prominence and advocacy by establishing joint business councils in un-served countries and re-activating dormant councils.

The PBC is a private sector not-for-profit advocacy platform set-up in 2005 by 14 (now 100+) of Pakistan’s largest businesses. PBC’s research-based advocacy supports measures which improve Pakistani industry’s regional and global competitiveness. More information about the PBC, its members, objectives and activities can be found on its website: www.pbc.org.pk

Download