Built on Rails: The State of Fintech in Pakistan

This report maps Pakistan’s fintech ecosystem as of 2026, its infrastructure, its principal segments, and the gap between explosive transaction...

This report maps Pakistan’s fintech ecosystem as of 2026, its infrastructure, its principal segments, and the gap between explosive transaction growth and genuine financial inclusion — benchmarked against relevant economies and drawing on interviews with senior industry practitioners.

The architecture of finance is being rewritten as Pakistan stands at an inflection point in its transition from a cash-based economy to a digital financial system. In little over a decade, paying, saving, borrowing, and investing have begun migrating from the bank branch and the cash counter to the mobile phone. A young population of more than 240 million, rising smartphone penetration, a sequence of ambitious regulatory reforms, and the rollout of national digital public infrastructure have made the country one of the more closely watched fintech stories in South Asia.

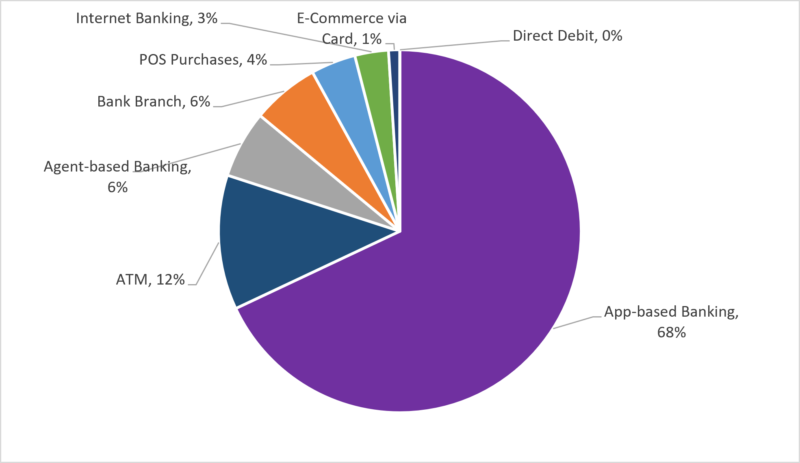

Pakistan’s digital payments have grown at remarkable speed. Retail payments reached 9.1 billion transactions worth PKR 612 trillion in FY 2025, and digital channels now account for 88% of retail transactions by volume, with mobile-app banking alone handling 6.2 billion transactions.

Pakistan Retail Payments Breakdown (FY 2025)

Source: Annual Payment Systems Review FY 2024-25, State Bank of Pakistan

At the centre of this shift is Raast, the SBP’s instant payment system, whose transaction volume has grown roughly 162-fold since 2022 at a CAGR of around 256%, reaching 1.28 billion transactions in 2025. User adoption has risen across every channel, with branchless-banking app users reaching 79.2 million and mobile-banking users 24.1 million.

Despite the growth in digital payments, cash continues to dominate by value, and Raast’s activity remains overwhelmingly person-to-person contributing 99% of volume and merchant payments remain very low. Even so, the prospect of digital payments fully replacing cash remains distant.

Pakistan’s position is best understood against comparable markets. The report benchmarks the country against India, Bangladesh, and Indonesia, the three economies that, alongside Pakistan, hold some of the world’s largest unbanked populations. On the most basic measure of inclusion, account ownership (aged 15+), Pakistan lags behind all three, at roughly 27% of adults against Bangladesh’s 43%, Indonesia’s 56% and India’s 89% — a gap that reflects how much of the rail-building is yet to convert into everyday use.

| Segment | Description | Binding constraints / Challenges |

|---|---|---|

| Digital Payments & EMIs | The most mature segment; digital channels carry around 88% of retail volume, with mobile apps processing over 6.2 billion transactions. Wallets such as Easypaisa and JazzCash dominate the segment, supported by Raast, PSOs/PSPs. EMIs have also emerged as a new category, they facilitate digital payments through e-wallets and cannot take deposits or lend. | EMIs earn only small per-transaction fees so it is difficult to generate profits. With no branches, customer service is the only human touchpoint and a key differentiator as providers scale. |

| Digital Banking | Full-service licensed digital retail banks (deposits, lending, cards, profit on balances) operating without branches, onboarding via NADRA biometric verification. This segment targets a young, digitally native population and many banks have attracted foreign capital reflecting external confidence in the opportunity. | Long road to profitability requiring patient investors; weak unit economics on low-balance customers. |

| Digital Lending (CreditTech) | An emerging, dynamic segment spanning across algorithmic nano-lending, earned-wage access and consumer finance, Shariah compliant Buy Now Pay Later (BNPL), and SME/supply-chain lending. AI-based scoring uses alternative data for near-instant decisions. | For new-to-credit customers, the binding constraint is the absence of a consolidated, API-accessible data layer to verify income, obligations and transaction history, forcing manual processes and limiting reach. |

| Microfinance | Both the institutional origin of Pakistan’s largest fintechs and the principal formal channel for low-income credit, with 10.5 million active borrowers — a rising share served via digital nano-loans. | Formalising the unbanked is hard: they are costly to acquire, generate low transaction volumes, and lack the data automated underwriting requires. |

| WealthTech & Capital Markets | Among the least-penetrated segments, with around round 500,000 investor accounts and 1.3 million total market investors. Investment platforms and mutual-fund distribution are widening access via digital onboarding, helped by a recent market rally. | Structural fragmentation: opening an account requires separately interacting with PSX, NCCPL, CDC and the investor’s bank, each with its own onboarding, documentation and often outdated technology. Some processes still mandate physical paperwork and settlement can take several days. |

| B2B & Supply-Chain Finance | A less visible but economically significant segment. Fintechs digitise invoicing, payments and distributor financing along supply chains, using in-chain transaction data as the basis for credit. | Scale and reach remain limited relative to the size of the SME financing gap. |

| Virtual Assets & Blockchain | The newest segment. Pakistan reportedly has one of the world’s larger crypto-using populations, which has for long remained in a regulatory grey zone. Pakistan Virtual Assets Regulatory Authority (PVARA) has been established which is empowered to license, regulate, and supervise virtual assets and providers. | For years, cryptocurrency trading and blockchain-based services operated in a regulatory grey zone being neither formally permitted nor clearly prohibited.

The segment’s trajectory depends heavily on the pace and clarity with which the new PVARA framework is implemented. |

Artificial intelligence can lower the cost of serving each customer through automated onboarding, fraud detection, and alternative-data credit scoring. Voice-based interfaces could bring finance within reach of the population that cannot easily read or write.

Cross-border remittances and stablecoins: Now backed with PVARA and Virtual Assets Act, blockchain-based settlement can offer near-instant, low-cost alternatives for remittances that accounted USD 38.3 billion in FY 2025.

Capital markets and WealthTech: Digital brokerages are resolving old barriers to entry issues by offering fully online onboarding, low minimum investments, and app-based trading aimed at a young, first-time investor base.

The report maps recommendations gathered through interviews and review of secondary data.

For regulators: scale open banking from sandbox to a full consent-based data-sharing layer; centralise and modernise the fragmented capital-markets back-end so investors are onboarded at once across different entities; and issue clear guidance on ethical, transparent AI.

For industry: Work towards bringing innovation rather than waiting for regulator-led innovation as the regulator has provided the framework and infrastructure, i.e., Raast, now the industry should build compelling use cases. Invest continuously in fraud prevention and consumer awareness; and pair merchant rollout with hands-on training.

For government: close the rural connectivity gap; reduce cash gradually by slowing note printing rather than abruptly demonetising; and embed financial and digital literacy in school curricula.

The PBC is a private sector not-for-profit advocacy platform set-up in 2005 by 14 (now 100+) of Pakistan’s largest businesses. PBC’s research-based advocacy supports measures which improve Pakistani industry’s regional and global competitiveness. More information about the PBC, its members, objectives and activities can be found on its website: www.pbc.org.pk

DownloadTelephone: 021-35630528-29

Fax: 021-35630530