Pakistan’s Readymade Garments Sector: Challenges and Opportunities

A Study Commissioned by the Pakistan Business Council The Pakistan Business Council (PBC) has commissioned CDPR to do this Study...

The Pakistan Business Council (PBC) has commissioned CDPR to do this Study as part of its Make-in-Pakistan initiative. The Make-in-Pakistan initiative of the PBC aims to reverse the premature deindustrialisation of Pakistan, this initiative aims to promote jobs, exports of value-added products, import substitution and increase revenues for the government.

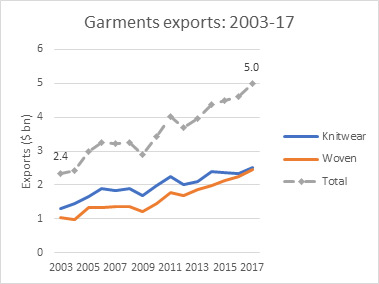

The textile is the most important sector of Pakistan’s economy. In 2017, it contributed almost 8.5% to the country’s GDP, accounted for one-fourth of industrial value-added and employed 40.0% of the industrial labour force. Amongst textile products, garments have the highest-value addition and is also the main export revenue earner. In 2017, Pakistan exported almost $5.0 billion worth of garments to the world: $2.52 billion (knitwear) and $2.47 billion (woven).

| Variable | Contribution of textiles to National Economy (%) |

|---|---|

| Share in GDP | 8.5 |

| Employment (share of industrial labour force) | 40.0 |

| Share in national exports | 60.0 |

| Share in industrial value addition | 25.0 |

| Share in large scale manufacturing | 21.0 |

Although garment sector exports have increased over the years and it has been the best performing segment of the textile value chain, the sector is grossly underperforming relative to its potential. Pakistan lags behind its competitors in the global share in export of garments. In 2017, Pakistan’s share in the exports of garments was a meagre 1.10% compared to China’s 32.06%, Bangladesh’s 7.66%, Vietnam’s 5.94%, and India’s 3.81%.

| Country | Garment Exports 2017 ($bn) | % share of world exports | Rank |

|---|---|---|---|

| China | 145.6 | 32.06 | 1 |

| Bangladesh | 34.8 | 7.66 | 2 |

| Viet Nam | 27.0 | 5.94 | 3 |

| India | 17.3 | 3.81 | 6 |

| Turkey | 14.8 | 3.26 | 7 |

| Cambodia | 11.3 | 2.49 | 10 |

| Pakistan | 5.0 | 1.10 | 17 |

| World | 454.2 |

The primary reason for this poor performance is the narrow export base, even this narrow base is biased towards low value-added unsophisticated items. The top 6 products exported by Pakistan account for 52.0% of Pakistan’s exports, but only 20.0% of total world garment exports. World demand has been shifting to man-made fibre, which Pakistan has been unable to exploit. In addition, Pakistan’s garment exports are not well diversified in terms of destinations. Almost 88.0% of garment exports are destined for the EU and the US.

Pakistan’s underperformance in exports can be attributed to a number of factors, divided into supply side, demand side and investment climate constraints.

Pakistan faces higher production costs and lower productivity compared to its peers. High production costs are in the form of import duty on cotton & MMF, high energy tariffs and minimum wage (Supply-Constraint). This has led to fierce competition with other low-wage competitors leading to small export orders for Pakistan (Demand-Constraint). Pakistan faces unfavourable tariffs in garment exports in the international market such as ASEAN, which restricts market access, and its currency in the recent past was overvalued with respect to the dollar, making exports less competitive against China, India, Bangladesh and Vietnam (Investment Climate Constraint). Other impediments include poor access to credit, delay in the payment of government-announced tax refunds, low technological adoption, and time-consuming export procedures.

This report proposes the following solutions to the above-mentioned problems.

Improve access & lower the cost of inputs: This can be achieved by improving ease of importing man-made fibers, removing extra taxes on utilities, establishing central bonded warehouses for better access to raw material and increasing labor productivity through training.

Encourage technology adoption: Measures include lowering duty rates on import of machinery and raw material for domestic manufacture, providing grants for sustainability initiatives and tax exemptions on innovation and R&D expenses.

Need appropriate and targeted industrial policy: Provide support to SMEs to encourage investment in ICT and ensure reliable supply of inputs and competitive credit.

CPEC: Use CPEC to leapfrog and climb the technology ladder in garments sector through joint ventures with Chinese companies that utilize Chinese expertise in RMG and Pakistan’s low cost labour.

Renegotiate better terms in Pak-China FTA: Concessions need to be more relevant for Pakistan. Products such as knitted/crocheted t-shirts, shirts and vests which are complementary in China’s imports and Pakistan’s export basket should be included in the FTA.

Improve access to credit by providing back-to-back L/Cs, corporate loan guarantees and export credit insurance.

Facilitate moving up the value chain by providing incentives for quality certifications, branding and marketing. Other schemes include providing matching grants or challenge funds to encourage upgradation of inputs.

Resolve problem of pending refunds under drawback schemes: Pay interest on pending refunds that have exceeded the permissible time limit. Incentives should be in the form of exemptions, rather than refunds.

Enhance role of industry associations: associations need to be given a bigger role in vetting of government policies and in defining sustainable targets.

The PBC is a private sector not-for-profit advocacy platform set-up in 2005 by 14 (now 78) of Pakistan’s largest businesses. PBC’s research-based advocacy supports measures which improve Pakistani industry’s regional and global competitiveness. More information about the PBC, its members, objectives and activities can be found on its website: www.pbc.org.pk

DownloadTelephone: 021-35630528-29

Fax: 021-35630530