“Enhancing the competitiveness of Pakistan’s Surgical Instruments Industry” is a joint study of the Pakistan Business Council (PBC) and the Engineering Development Board (EDB) with support from the Surgical Instruments Manufacturers Association of Pakistan (SIMAP). The study is part of the PBC’s Make-in-Pakistan initiative and is based on existing secondary data / research on the sector supplemented with field interviews of firms in the Surgical Instruments manufacturing cluster located in Sialkot – Pakistan.

Global Surgical Instruments Industries:

The US FDA has classified medical devices into three categories: Class I, Class II and Class III depending on their risk and criticality. Examples of Class I devices are tongue depressors, bandages, gloves, bedpans, and simple surgical devices. Examples of Class II devices are wheelchairs, X-ray machines, MRI machines, surgical needles, catheters, and diagnostic equipment. Class III devices are used inside the body and include heart valves, stents, implanted pacemakers, silicone implants, and hip and bone implants. Surgical Instruments can also be classified under two major usage categories: disposables and non-disposables.

Most of the world’s surgical instruments are made by firms in selected cities & towns in Europe and Asia—these locations include Tuttlingen (Germany), Sialkot (Pakistan), Penang (Malaysia), Debrecen (Hungary), and Warsaw (Poland).

Pakistan’s Surgical Instruments Industry:

Pakistan’s Surgical Instrument manufacturers mainly produce Class I and some Class IIb instruments.

The Surgical Instruments industry of Pakistan is a highly fragmented industry, with a strong export orientation, operating in the city of Sialkot, in the Punjab province of Pakistan. The industry consists of a multitude of small and medium sized manufacturers with a few large units. The industry mostly operates on an OEM (Original Equipment Manufacturer) model. Orders and specifications are received from buyers, mostly in Germany, UK and the USA.

Local manufacturers construct the product according to specifications and export these to the overseas buyers who usually brand the instruments and supply them to distributors overseas. Pakistan’s market share of surgical instruments has remained nearly static at 0.7 over the last 10 years suggesting a strong correlation of 0.96 with world demand.

| Exports of HS-901890 Surgical Instruments |

| Value in USD Mn |

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

| World |

34,126.5 |

36,883 .9 |

41,192.9 |

42,414.5 |

45,181.5 |

47,765.0 |

45,796.2 |

47,605.5 |

50,005.7 |

54,619.2 |

57,825.3 |

58,112.2 |

| Pakistan |

233.0 |

219 |

271.7 |

291.4 |

296.8 |

319.5 |

332.6 |

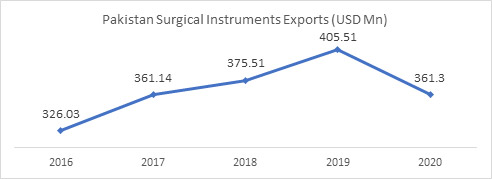

326.0 |

361.1 |

375.5 |

405.5 |

361.3 |

| %age share of Pakistan |

0.7% |

0.6% |

0.7% |

0.7% |

0.7% |

0.7% |

0.7% |

0.7% |

0.7% |

0.7% |

0.7% |

0.6% |

| Source: (International Trade Center, 2020) |

The German SME surgical instrument manufacturers, who are the world leaders in surgical instruments, have mostly outsourced the lower technology intermediate and end products to the Sialkot cluster. While Pakistan’s surgical instruments industry remains competitive in the low-tech end of the product scale, its exports are highly concentrated in a few geographical areas primarily because of established supply chains and the difficulties involved in entering new markets.

The top 3 destinations for Pakistan’s surgical instruments are the USA, Germany and the UK. Nearly 80% of surgical instruments made in Pakistan are exported to 15 countries. This limits Pakistan’s export potential and increases concentration risk.

Major Findings:

- Our findings indicate that the surgical industry, despite being in existence for a long time, is not performing to its full potential. Compounded Annual Growth Rate from 2016-2020 was 2.6%. Despite the lack of fiscal space, the Government of Pakistan has been giving incentives to the industry to grow, however, the full development and export potential of the industry is yet to be realized. It is becoming increasingly clear that the government and industry need to come up with a joint strategy which encompasses product, process and new market development if the industry is to achieve its potential.

- Pakistan’s market share in the global trade for surgical Instruments is only 0.7%. The low market share in terms of value appears to be primarily due to the absence of continuous product & process innovations aimed at producing products which fetch higher prices in global markets.

- There is intense competition in Sialkot. Most local producers cite each other as their major international competitors. Although local rivals claim to compete based on product quality, the primary basis of competition appears to be price.

- There is an absence of stamping of Made-in-Pakistan on export products, no major Pakistan brands and hence no country-of-origin advantage. The industry is neither branding nor stamping instruments with the ‘Made in Pakistan’ label when exporting to Europe. Sometimes exporters put the ‘Made in Pakistan’ label on the carton but not on the instruments themselves.

- Buyers in the Middle Eastern market prefer to buy Pakistani instruments from US or European suppliers but not directly from Pakistan. This is because of their trust in European and American brands even though Pakistani manufacturers are OEM suppliers. Industry players in Sialkot need to appreciate the importance of brand building which can allow them to charge a premium. In addition to strong brands, country-of-origin association between Pakistan and Surgical Instruments will also facilitate Pakistani suppliers to enter new markets.

- The Pakistani Surgical Instruments industry will face a new challenge in the form of the Medical Device Regulation (MDR) to be mandatorily introduced in the EU beginning 2024. All instruments destined for the EU will have to be compliant with the new European regulations on biocompatibility. The new regulations are expected, at least in the initial period to hinder exports of Surgical Instruments to the EU.

Major Recommendations:

- There is potential for Pakistani manufacturers to enter into JVs with German or Chinese firms. The country has a population base of 220 million and approximately 2,000 hospitals, which offer a potential market for 17 million surgeries per year, these JVs can rapidly build, scale and enter export markets.

- For the upcoming MDR compliance of the EU, The Government may bring in foreign consultants for a limited time to assist in MDR compliance. Any cost of hiring consultants, building a lab etc. should be reflected in the pricing of the instruments that need compliance with MDR. If prices do not reflect the costs associated with compliance with MDR, the Pakistani taxpayers might end up subsidizing consumers in the EU.

- To improve product quality and consistency, the industry will need to self-regulate. Some options could include: provision of raw materials from a central SIMAP warehouse, SIMAP approved certification requirements for exporters, lobbying with the government to ensure that minimum export prices reflect costs of inputs etc.

- On the marketing end, Pakistan could learn valuable lessons from the Turkish “TURQUALITY” Program through which the Turkish government has been funding the development of 10 worldwide Turkish brands. A “PAKQUALITY” initiative may be promoted under the Public Private Partnership model to ensure that Pakistani brands also become regional / global icons.

- To make the product more presentable, the manufacturers may create kit packages similar to China.

- The minimum export price may only be reduced for disposable instruments, not reusable ones. To prevent misuse of the proposed change, one option could be the implementation of Global Devices Medical Nomenclature (GMDN) for identification of instruments. GMDN is a system of internationally agreed generic descriptors used to identify all medical device products.

- To diversify concentration risk, PBC has identified that the East African countries and South Africa are potential markets where TDAP may look to hold more exhibitions. Other potential markets include Canada and the ASEAN region. EDB needs to work with the Association to create awareness regarding compliance requirements in new markets, and help manufacturers comply with these requirements.

- While the Surgical Industry is proposing that the government build a new Common Facility Center, complete with the latest machinery, PBC proposes that the existing Common Facility Center may be upgraded with among others newer heat treatment furnaces, newer CNC laser cutting machines etc., and if this is not possible in the existing setup, a new CFC run by SIMAP may be set up.

- E-commerce platforms such as Alibaba, Amazon etc. may be utilized as sales channels. Sellers in other countries such as China and Vietnam use e-commerce platforms. Use of alternative sales channels also reduces over-reliance on exhibitions and commercial counsellors, many of whom are not subject experts on Surgical Instruments when dealing with foreign buyers.

- Currently, Pakistan has one of the highest documentary compliance rules compared to other countries. Increased documentation hurts business and therefore revenues. Pakistan needs to simplify its documentation process and do away with needlessly complicated bureaucratic procedures. Other nations require far less documentary compliance and as a result have less cost to export which promotes an export-friendly environment.

The PBC is a private sector not-for-profit advocacy platform set-up in 2005 by 14 (now 89) of Pakistan’s largest businesses. PBC’s research-based advocacy supports measures which improve Pakistani industry’s regional and global competitiveness. More information about the PBC, its members, objectives and activities can be found on its website: www.pbc.org.pk

Download